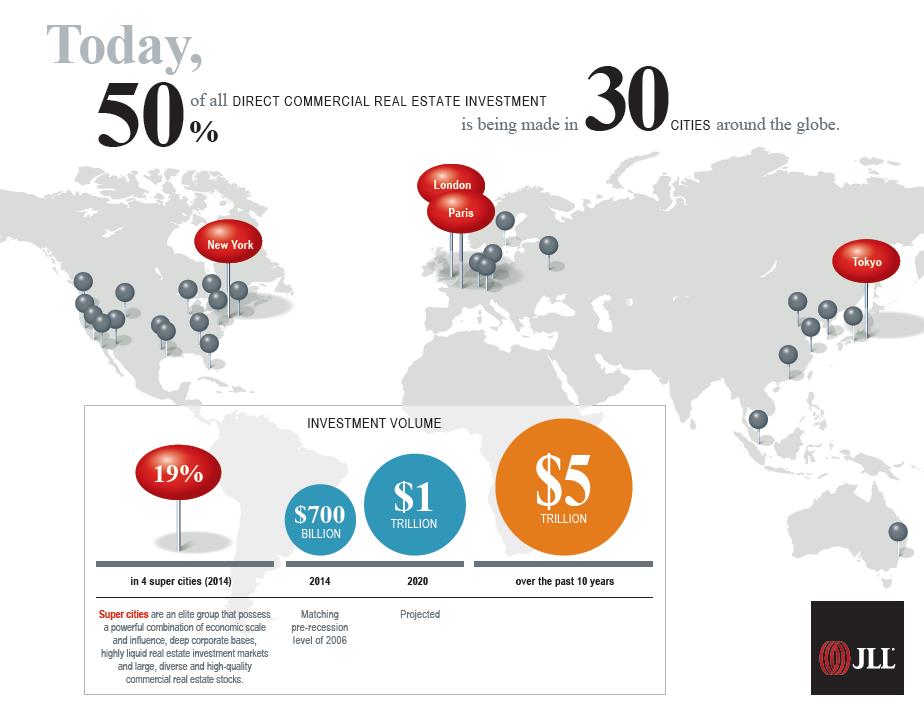

Research by JLL shows that as real estate investment reaches pre-recession levels, 50 percent continues to be concentrated in 30 cities worldwide

CHICAGO and LONDON, January 21, 2015 — An analysis

of the top cities for real estate investment continues to demonstrate

the contribution of real estate to the success of established and

emerging cities across the globe. According to research by JLL

(NYSE:JLL), total direct real estate investment is expected to have

reached US$700 billion in 2014, matching the pre-recession levels of

2006, and is projected to increase a further 5-10 percent in 2015 driven

by a robust economic environment.

As business and political leaders convene to discuss global issues at the World Economic Forum annual

meeting in Davos, Switzerland, there is a greater appreciation for the

importance of real estate in the global context. A look at the 30

cities worldwide where 50 percent of the US$5 trillion in direct

commercial real estate investments has been concentrated over the past

decade highlights the impact of real estate investment and investor

confidence on the strength of super cities and the growth of second-tier

cities. This is particularly evident in the four super cities – London,

New York, Paris and Tokyo -- where one of every five dollars of

commercial real estate transactions took place, representing 19 percent

of total global volumes.

According

to Colin Dyer, CEO of JLL: “As real estate investment reaches the

levels last seen before the Great Financial Crisis, we are optimistic

about the positive impact of these investments on cities, in part, due

to the improved underwriting practices that have been put in place in

the last few years. We expect investments to continue to grow because

the market is on a sounder footing than it was before the recession and

has more robust controls and scrutiny on investments.”

According

to Colin Dyer, CEO of JLL: “As real estate investment reaches the

levels last seen before the Great Financial Crisis, we are optimistic

about the positive impact of these investments on cities, in part, due

to the improved underwriting practices that have been put in place in

the last few years. We expect investments to continue to grow because

the market is on a sounder footing than it was before the recession and

has more robust controls and scrutiny on investments.”

Direct real estate investment is expected to continue increasing to approximately US$1 trillion by 2020 driven by:

- Improved

controls including reduced reliance on leverage, greater use of equity,

stricter under-writing standards and increased scrutiny by investment

committees

- The emergence of new sources of capital, primarily in Asia and other emerging economies

- Increased

allocation to direct real estate from institutional investors in

developed markets due to low interest rates and an evolving regulatory

environment

- Growing cross- border investments from South Korea,

China, Taiwan and Malaysia spurred by government efforts to reduce

domestic overexposure by moving capital offshore

Recent research from

JLL identifies the continued importance of the four global super cities

while second-tier tech rich cities in Europe and the United States grow

and attract investors.

• The dominance of the super cities for

total and cross-border investment in 2014 was driven partly by single

asset mega-deals – such as the Gherkin and HSBC office towers in London,

Pacific Century Place office tower in Tokyo, the Waldorf Astoria hotel

in New York and the Marriott Champs Elysees hotel in Paris.

Interestingly, two of these deals were secured by

high-net-worth-individuals, an emerging class of investors who are able

to challenge and beat institutions for trophy assets in the main global

cities.

• The underlying shift in investor activity toward

second-tier cities also continued. This is most apparent in Europe

where, for example, the number of transactions in London and Paris fell

by 17 percent year over year, but increased by 37 percent in the next 20

largest investment destinations.

• In Northern Europe, mid-sized

cities – notably Dusseldorf, Hamburg and Munich (Germany), Amsterdam

(Netherlands), and the Nordic capitals of Oslo and Copenhagen –

experienced high levels of investment volumes as a proportion of city GDP.

These transparent and stable real estate markets with strong technology

and environmental credentials are attractive to corporate tenants and

investors.

• In Europe, investment volume growth also extended to

cities such as Dublin and Madrid, which were considered almost

un-investible just a few years ago. Dublin jumped to 24 in the global

investment hierarchy from 93 in 2013 and has the world’s fastest growth

in office rents over the past year.

• In the U.S., transaction

volumes shifted to the primary gateway cities of New York, Los Angeles,

Chicago, San Francisco, Washington, D.C. and Boston, reversing a trend

toward secondary cities seen in 2012 and 2013. Commercial real estate

investment volumes in primary cities were up 66 percent year over year,

compared with 37 percent for the U.S. market as a whole.

• Some

U.S. secondary markets such as Philadelphia, Miami and Charlotte did

experience increased interest from domestic institutional buyers.

Foreign buyers, on the other hand, are not as active in most secondary

cities yet outside of trophy, core-plus deals. Transaction volumes in

secondary cities are expected to increase in 2015 driven by an increase

in assets for sale.

• Most pan-Asian investment was focused on the

major cities of Tokyo, Sydney, Melbourne, Hong Kong, Singapore, Seoul,

Shanghai and Beijing. With a lack of volume growth across the region in

2014, there was less appetite for secondary city opportunities outside

of trophy or core opportunities due to lower transparency and market

accessibility.

• Multi-family assets have been a focus of

investor activity in the U.S. and interest in these properties has

spread to countries such as the UK and Australia. Additionally, Chinese

residential developers have expanded aggressively into overseas markets

in recent years, with a focus on London, New York, San Francisco,

Toronto and Sydney.

About JLL

JLL (NYSE: JLL)

is a professional services and investment management firm offering

specialized real estate services to clients seeking increased value by

owning, occupying and investing in real estate. With annual fee revenue

of $4.0 billion and gross revenue of $4.5 billion, JLL has more than 200

corporate offices, operates in 75 countries and has a global workforce

of approximately 53,000. On behalf of its clients, the firm provides

management and real estate outsourcing services for a property portfolio

of 3.0 billion square feet, or 280.0 million square meters, and

completed $99.0 billion in sales, acquisitions and finance transactions

in 2013. Its investment management business, LaSalle Investment

Management, has $53.0 billion of real estate assets under management.

JLL is the brand name, and a registered trademark, of Jones Lang LaSalle

Incorporated. For further information, visit www.jll.com.

Contacts