Strong returns, fair value and more debt help to put Europe at the top of international hotel investors’ wish list according to research from JLL Hotels & Hospitality Group

The Europe, the Middle East and Africa (EMEA) hotel investment market is set for another bumper year according to research undertaken by JLL’s Hotel & Hospitality Group.

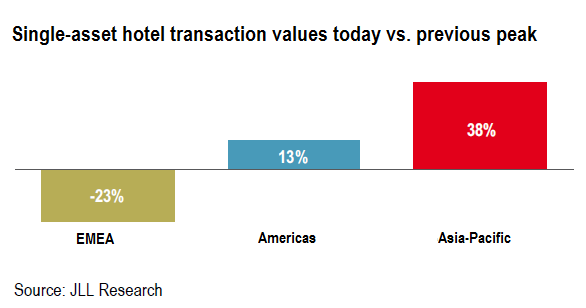

EMEA

is projected to see close to $25 billion in hotel trades in 2015 – up

from $21.5 billion in 2014 and representing 36% of all hotel

transactions globally.

Much of this activity will be driven by

large single-asset transactions, led by London and Paris, while

portfolio deals are anticipated in the U.K. and Germany.

Global

hotel real estate transaction volumes are expected to reach $68billion

in 2015 with global funds and private equity groups based in the U.S.

and Western Europe leading the charge. The U.K., Germany and the US

represent the biggest destinations for private equity capital globally.

Asian

money will also feature more strongly in 2015, especially driven by

Chinese capital. Asian insurance companies have helped grow the swell of

outbound capital from several hundred million dollars annually during

the past several years to nearly $1 billion in 2014. Global cities with

direct flight connections to China such as London, Paris, Amsterdam,

Dubai are high on investors’ wish lists.

Attractive yields

North

American private equity funds have cash to deploy in the short term and

European yields remain some of the most attractive – especially at a

time when prices continue to rise on home soil.

“Whilst the question

of fair value resounds through the sector, Europe still offers more

upside on the recovery curve, with per-key values of assets still below

the previous peak in both Western and emerging Europe. In 2015, we will

see private equity investors look to higher yielding markets such as

Southern and emerging Europe, as investors continue to follow

opportunities.” Said Christoph Härle CEO EMEA, JLL Hotels & Hospitality Group.

“Many

European countries have additionally reached their occupancy ceiling.

Thus, average rates will be the key driver of RevPAR moving forward,

boding well for hotel profit increases. The Middle East is expected to

see growth as well, and hotels in Africa will at times experience

double-digit RevPAR growth.” Said Härle.

Opening up of debt

Last

year saw debt opening up in a controlled manner in the Eurozone as

balance sheet lenders made their way back into the hotel lending space.

“2015

will mark the redemption of Commercial Mortgage-Backed Securities

(CMBS) market as a debt investment product, in the UK and Continental

Europe. With improved underwriting standards and increased subordination

levels, we expect bond investors to accept hotel assets as underlying

security again, closing some of the funding gap in the space. The return

of CMBS will provide potential for growth, which will help support the

growing investor demand for acquisitions in EMEA and will stretch equity

further. In addition, direct lending funds (Shadow-banks) are

increasingly closing the LTV gap between the current 50%-55% senior

position and the 75% LTV. More push from capital exporters in China and

the Middle East will put an upward pressure on deal flow as well.” Continued Härle.

– ends –

Contact Us